2018 has been an interesting and volatile year for natural gas in the United States. 2017 saw us quadruple our liquefied natural gas exports, and 2018 has been quite similar with exports up 8% in the first quarter. Projections indicate that the U.S. is likely to be a net exporter of natural gas in 2018, something that was achieved for the first time in 2017. This was also a time of surging production; EIA projects that natural gas production will average 80.5 billion cubic feet per day (Bcf/d) in 2018, an increase of 9.4% year-over-year.

However, this record production was met with surging demand over the first half of the year. While production levels reached record highs, an incredibly cold and long winter (extending into April) ate into natural gas storage levels. In the first half of 2018, there were 17% more heating degree days (days in which power consumption largely went towards keeping homes and businesses warm during winter lows) than there were in the first half of 2017. It was not until April 27th that winter weather subsided enough to cease withdrawing natural gas from storage, and begin depositing, or injecting, it. In the EIA’s recorded history (dating back to 1993) there have never been three consecutive withdrawals from storage in April until this year. We ended the winter season with rather low natural gas storage levels.

In this article, we’ll take a close look at the factors and trends affecting the natural gas industry, both supply and demand. We’ll also forecast the factors on the horizon, as we approach 2019, and determine how the industry may shift in the near future.

Supply Factors

The general supply-side factors affecting natural gas prices are typically identified as production, imports, and storage levels. As mentioned above, this was a volatile year for natural gas supply; a time of surging production, but also surging exports and heavy demand taking a severe toll on storage.

Production

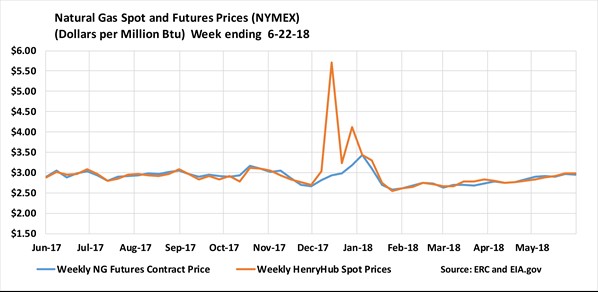

Natural gas production sustained significant growth this year, repeatedly breaking production records week after week. This is in large part due to drilling in the Marcellus Shale region, the Permian, and gas as a by-product of oil drilling. The effect of this record production was incredibly pronounced; though 2018 gave us a long, cold winter, the sustained escalation of production kept pace with the unexpectedly high demand. As such, the Henry Hub spot price (the typical benchmark price that is often evaluated as the price of natural gas in North America) frequently failed to break $3 per million British thermal unit or MMBtu. This price is typically seen as psychological, but an important indicator of the state of natural gas.

If record natural gas production continues, businesses and residences in much of the U.S. will continue to enjoy lower utility bills, driving business growth and aiding in our economy.

Imports

The United States has continued on-trend to be a net exporter of natural gas, and EIA projects that trend will only continue and expand. However, we still import natural gas, mostly from our neighbors to the north in Canada.

As production increases, importation decreases. That’s a natural relationship, we’re making more so we need to purchase less. Typically, natural gas imports are highest in the winter, when domestic demand is at its greatest, and comes via pipeline from Canada, and occasionally in the form of Liquefied Natural Gas (LNG) from Trinidad.

Overall, it is likely that imports shall only continue their freefall as production surges.

Storage

Storage is naturally a by-product of supply and demand, but it also serves as a balance and a factor for pricing in and of itself. When storage levels are low, prices typically increase as a natural reaction of supply and demand. Due to the long winter, natural gas storage levels ended the winter withdrawal season roughly 30% lower than the five-year average, which is the baseline for judging storage health. The injection season began in late April, much later than usual. However, injections proved strong through June, and the first month of early Summer ended with a storage deficit of 19.5% compared to the five-year average, which, while still lower than the five-year average, is sufficient for summer demand.

Demand Factors

The demand-side factors influencing natural gas prices are typically identified as the weather, economic growth, and the availability and prices of competing fuels. This was certainly a year that emphasized the first two factors especially, though the third certainly played its role. We had one of the coldest winters on record in 2017-2018, with several record lows broken across the country, and manufacturing, the industry we most associate with economic growth-driven energy demand, has had a banner year in 2017 and 2018.

Weather

No doubt about it, 2017 and 2018 provided us with some extreme weather conditions. It cannot be emphasized enough how profound the effect of prolonged winter was on generating winter heating demand.

While temperatures remained cold in April, a saving grace was that May proved fairly mild, and June reasonable, allowing for recovery of natural gas storage levels.

As usual, weather remains the most volatile factor for natural gas prices; it is often vaguely predictable at best, and seems to constantly thwart any attempt for definitive forecasting.

Economic Growth

It should surprise no one to say that businesses need power. The busier we are, the more power we need, and both 2017 and 2018 have been banner years for business, especially in the field of manufacturing. 2017 was the most productive year for manufacturing since 2011, and 2018 is not far behind. There exists a bit of a push-pull effect between natural gas costs and manufacturing, as well. When prices are low, as they have been, it encourages the expansion of manufacturing, which in turn increases consumption.

All in all, if policies prove to be successful in luring manufacturing to the United States, it will absolutely be a driver of natural gas consumption, and thus promote upward pressure on natural gas prices. This article will not seek to delve into the impact of taxes, tariffs, or trade deals, as those topics are best left to economists and qualified analysts. Suffice it to say that this factor is largely influenced by GDP growth, productivity, technological advancements, and trade policy.

Competing Fuels

In April 2015, more electricity was generated from natural gas than from coal for the first time on a monthly basis, and in 2016, on an annual basis. 2017, similarly, saw natural gas generate more electricity than coal for the second consecutive year. Advancements in energy efficiency have made it less taxing to generate natural gas than coal, as well as less carbon-intensive. Despite coal generating less electricity than natural gas, it produced twice as much CO2.

Natural gas’s increased availability, lower prices, and general environmental advantages have made it a go-to fuel. In forecasting the future, factors to watch for include administrative policy or technological breakthroughs. At the beginning of 2018, FERC declined Energy Secretary Perry’s request for a grid resiliency plan to require utilities to buy above-market rate electricity from coal and nuclear providers. If, in the future, the DOE successfully enacts policies that subsidize coal or nuclear power for the purposes of making it competitive with natural gas, that would absolutely affect natural gas consumption.

The Future

In summation, as we look forward to natural gas in 2019, policy and production will likely be the factors to watch. Of course, weather-based demand will continue to serve as a fundamental driver of natural gas prices, and should not be ignored. As in 2017, 2018 has exemplified the staying power of the shale revolution, which among other factors, brought the United States an era of lower power prices. As businesses become more efficient, production increases, and economic growth continues, we should expect 2019 to be an interesting year for the natural gas industry.